Geopolitical tensions between the US and Iran may pose additional risks to the global dairy market, although the direct impact on dairy trade remains limited for now. The main consequences are related to rising energy costs, logistics, and international trade financing.

Geopolitical tensions and logistics

The escalating situation in the Persian Gulf region is driving up oil prices and creating risks for shipping through key sea routes. As a result, freight costs, cargo insurance, and transportation costs to the Middle East and South Asia may increase.

For the dairy sector, this means an increase in the final cost of imported products, especially in markets that are dependent on imports. In such conditions, suppliers located closer to the markets may gain a certain advantage. In particular, European producers may strengthen their position in the markets of North Africa and the Middle East compared to suppliers from Oceania or the United States.

In addition, rising energy prices are exacerbating global inflationary pressures and may lead to higher interest rates. This, in turn, increases the cost of financing international trade, which is particularly noticeable for expensive goods such as dairy products.

Dairy market: various trends

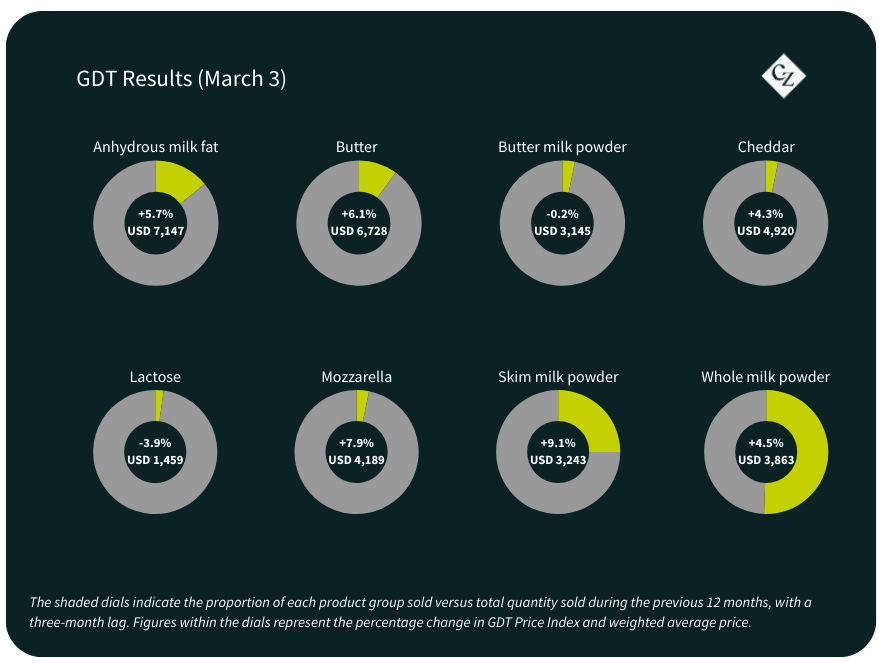

At the first GDT event in March, prices rose by 5.7% over the month, marking the second consecutive increase in 2026. The average winning price was $4.30, with the largest increases observed in the dry milk, cheese, and butter segments.

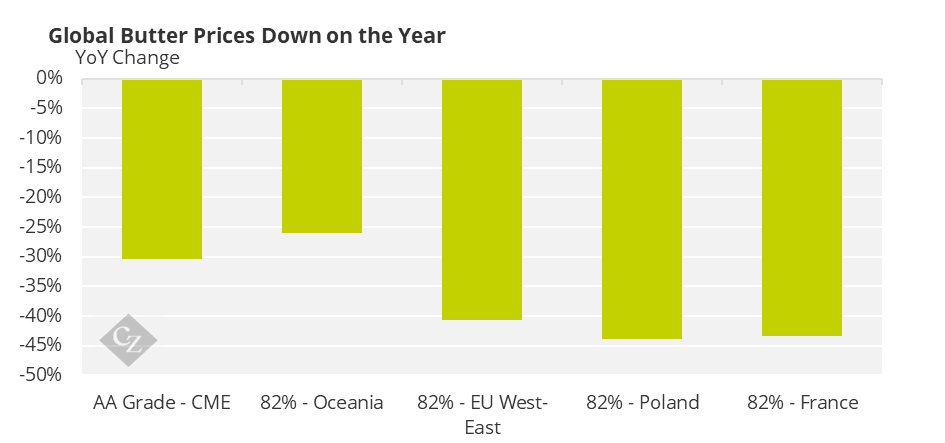

Despite the increase, global butter prices from CLAL in January-February 2026 were around €4,150/ton, significantly below the peak level at the end of 2024, which exceeded €7,000/ton, confirming a deep correction in fat content.

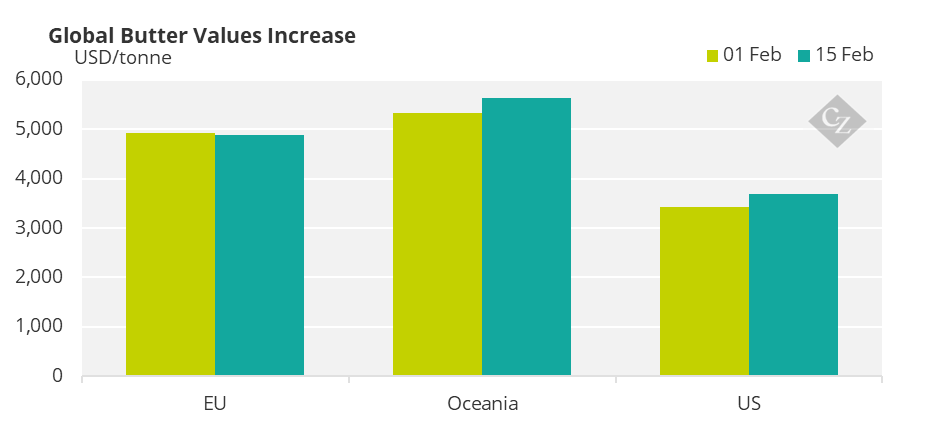

Data from the European Commission confirms this. The price of butter in the EU fell by 1.1% between February 1 and 15 to US$4,873 per ton, while the price of butter from Oceania rose by 5.6% to US$5,625 per ton, widening the gap between the EU and Oceania.

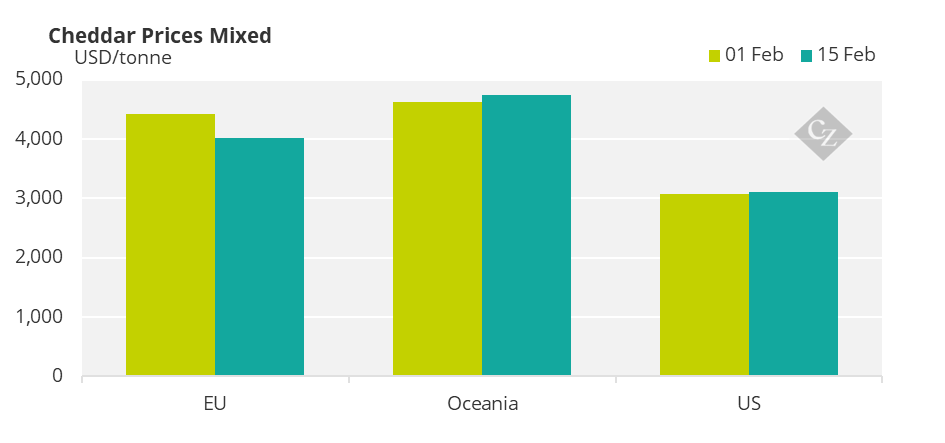

Cheese prices in the EU have also fallen in recent weeks, while Oceania and the US have seen increases. The European Commission reports that cheese in the EU fell by 9.3% from February 1 to 15 to US$4,012 per ton, while the price of cheddar cheese in Oceania and the US rose by 2.4% to US$4,738 per ton and by 1.2% to US$3,111 per ton, respectively. Block cheese from the US showed a moderate recovery but remains historically cheap in real terms, exacerbating global cheese difficulties.

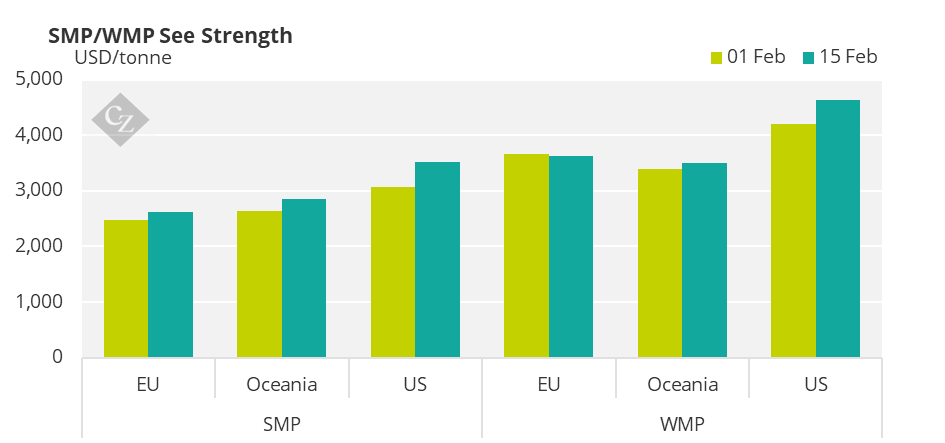

Powdered dairy products are increasingly attracting market attention. In the last two weeks alone, the price of skimmed milk powder (SMP) in the EU has risen by 5.8% to $2,616/t. In Oceania, the increase was 8.5% (to $2,863/t), and in the US, the price jumped by 15.1% to $3,526/t. At the same time, a significant increase in price was also observed for whole milk powder (WMP) in all key regions.

Recent events at Global Dairy Trade (GDT) have demonstrated more confident pricing for SMP and WMP. This confirms the assumption that powdered dairy products may be the first to begin a gradual market recovery after a sharp drop in prices at the end of 2025.

Despite the fact that the global market remains oversaturated with milk, a significant portion of it is currently being used for the production of cheese and whey. As a result, relatively little additional raw material is available for the manufacture of products such as skimmed milk powder, which is supporting price growth in this segment.

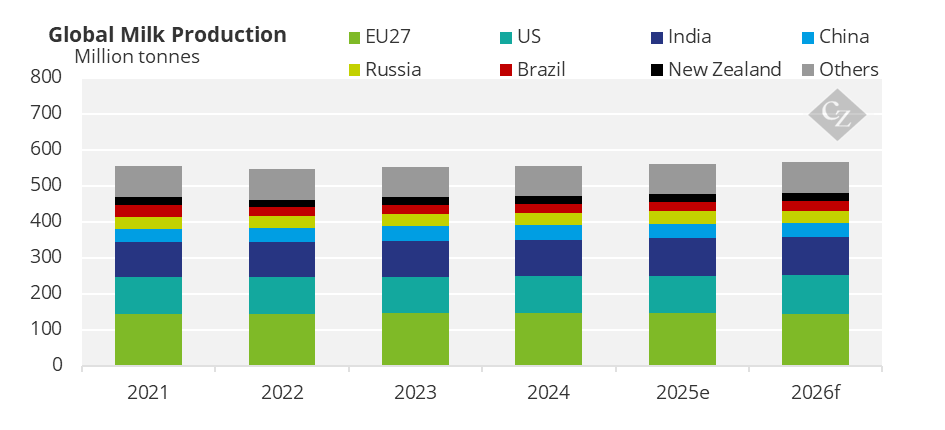

Surplus milk on the world market

Global trade in dairy products in February 2026 continues to reflect the situation of excess milk supply. According to the AHDB review, milk supplies from major exporters remain more than 4% higher than last year, exacerbating the structural surplus and shaping global trade flows.

The EU remains one of the most active exporters. Supplies of milk powder and cheese to foreign markets remain high thanks to competitive prices and logistical advantages in trade with North Africa and the Middle East. Since European butter and milk powder are often cheaper than their Oceanian counterparts, price-sensitive buyers are increasingly choosing EU suppliers.

The US is also increasing exports thanks to growth in milk production and expansion of cheese production capacity. Larger volumes of American cheese, whey, and milk powder are being directed to foreign markets, primarily Mexico and Southeast Asia, although global oversupply is holding back significant price increases.

At the same time, Oceania remains a benchmark for the milk powder market, but its traditional dominance is gradually weakening. Small price differences between products from Oceania and the EU allow buyers to quickly change the origin of goods, while increased transportation and insurance costs, exacerbated by geopolitical tensions, are contributing to a shift in demand from the Middle East and North Africa to European suppliers.

Arbitrage and spot opportunities remain limited but still exist in the market.

Arbitrage and spot opportunities in the market remain limited, but are still present. A small premium on butter and milk powders from Oceania compared to EU prices creates certain opportunities for arbitrage in Asian markets. At the same time, European cheeses for breakfast and culinary use may be offered at lower prices than products from Oceania in certain tenders, especially where logistics and quality requirements allow.

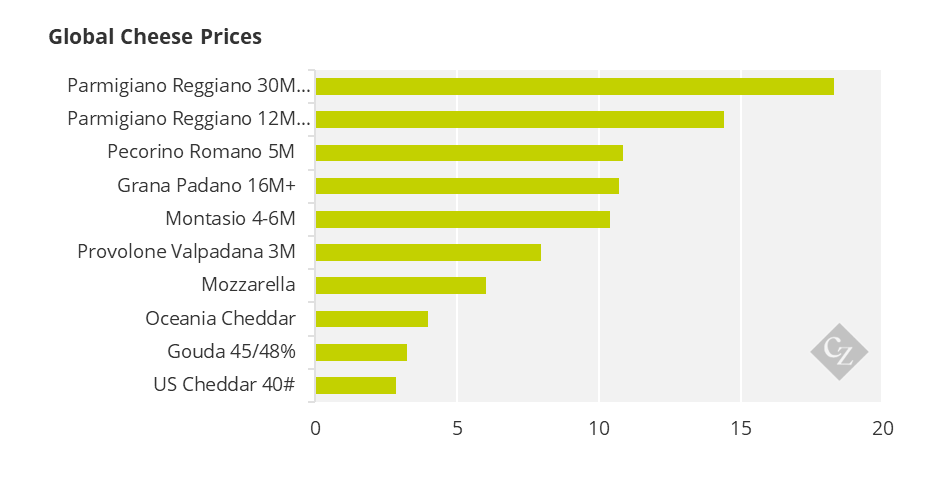

In Europe itself, according to CLAL, cheese prices remain relatively high. In particular, Gouda is trading at around €3.20–3.30/kg, while milk fat is cheaper. At the same time, Italian hard cheeses, in particular Parmigiano-Reggiano, remain at traditionally high price levels.

This contributes to a partial redirection of milk from butter and milk powder production to the cheese segment. As a result, the availability of milk fat at the processing stage is reduced, which may support a short-term recovery in butter prices, especially during periods of limited fresh cream supply.

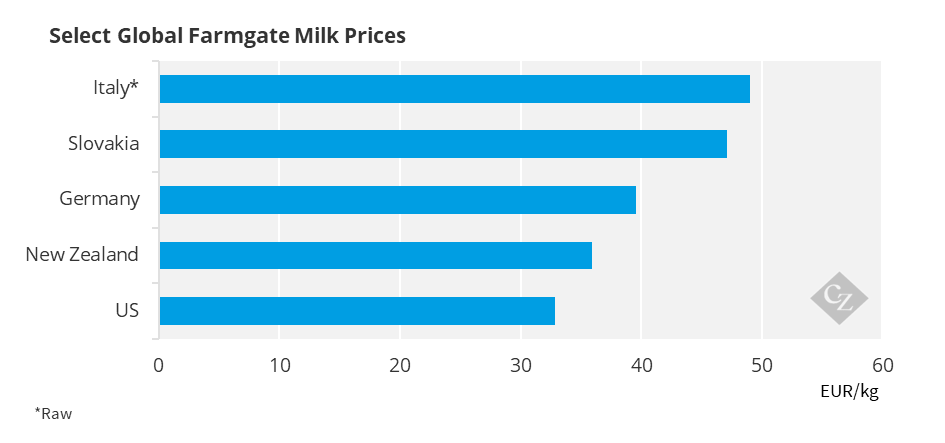

At the same time, spot milk prices, according to CLAL data in Italy and Germany, have already fallen from their peak levels in 2025, but in some weeks remain higher than the equivalent of dry milk. This indicates that local demand for drinking milk and cheese continues to actively absorb raw materials, limiting the volumes of milk available for export-oriented drying capacities.

Under such conditions, short-term arbitrage may arise for SMP and WMP exporters when price increases on the GDT auction outpace spot price adjustments in the EU.

The “milk tsunami” is facing weaker demand

The global dairy market continues to be characterized by significant milk supply amid moderate demand, so price stabilization remains fragile for now. Rabobank’s quarterly report notes that milk production is growing in most key exporting countries, primarily in the EU, the US, and New Zealand. This is holding back a sustained rise in prices, even despite the recent increase in quotations for milk powders and fats from Oceania.

Analysts are increasingly referring to 2026 as the year of the “milk tsunami,” meaning not a short-term surge, but a structural oversupply. Production is increasing in the EU, the US, New Zealand, and Argentina, while Australia remains the only major producer where milk volumes are steadily declining on an annual basis.

Demand is growing more slowly

Despite stable production, demand for dairy products is growing more slowly. In developed countries, per capita consumption of drinking milk is gradually declining, while demand for cheese and high value-added products remains relatively stable.

In developing countries, particularly in Asia and the Middle East, demand for milk powder and affordable dairy products continues to grow, but growth rates remain lower than before 2020.

As a result, the global dairy market is currently experiencing oversupply, which limits the potential for sustained price growth, especially for fats and bulk dairy products.

Source: CZ App (Czarnikow)