Roland Berger reports that the German dairy industry is facing a paradigm shift. Fluctuations in raw material prices, accelerated structural changes, growing pressure on margins in the raw materials business, and technological progress driven by artificial intelligence are fundamentally changing the rules of the game in the sector.

Drawing on Roland Berger’s industry expertise and in-depth market analysis, they have formulated six scenarios for the development of the German dairy sector in the coming years. These scenarios clearly outline what companies need to do now to secure or strengthen their competitive positions.

Hypothesis 1: Volatility is the new normal

Milk prices in Germany are subject to increasingly pronounced cyclical fluctuations. By the end of 2025, the price of raw milk had fallen by more than 30 per cent in just four months – with the decline in southern Germany being significantly slower than in the north.

There are numerous reasons for this: contrary to forecasts, there is currently a significant surplus of raw milk. Feed costs account for approximately 50 to 60 per cent of the cost of milk, which is highly sensitive to geopolitical trade restrictions. Energy costs have also recently risen sharply again – European gas prices rose by more than 38 per cent in a single day.

As around half of Germany’s milk production is exported, the market is directly exposed to geopolitical risks. This makes it all the more important for companies to develop forecasting excellence and responsiveness as key strategic competencies – combined with a solid own-base to help absorb fluctuations in revenue. Roland Berger supports them in these efforts through industry expertise and AI-based planning models for proactive volatility management.

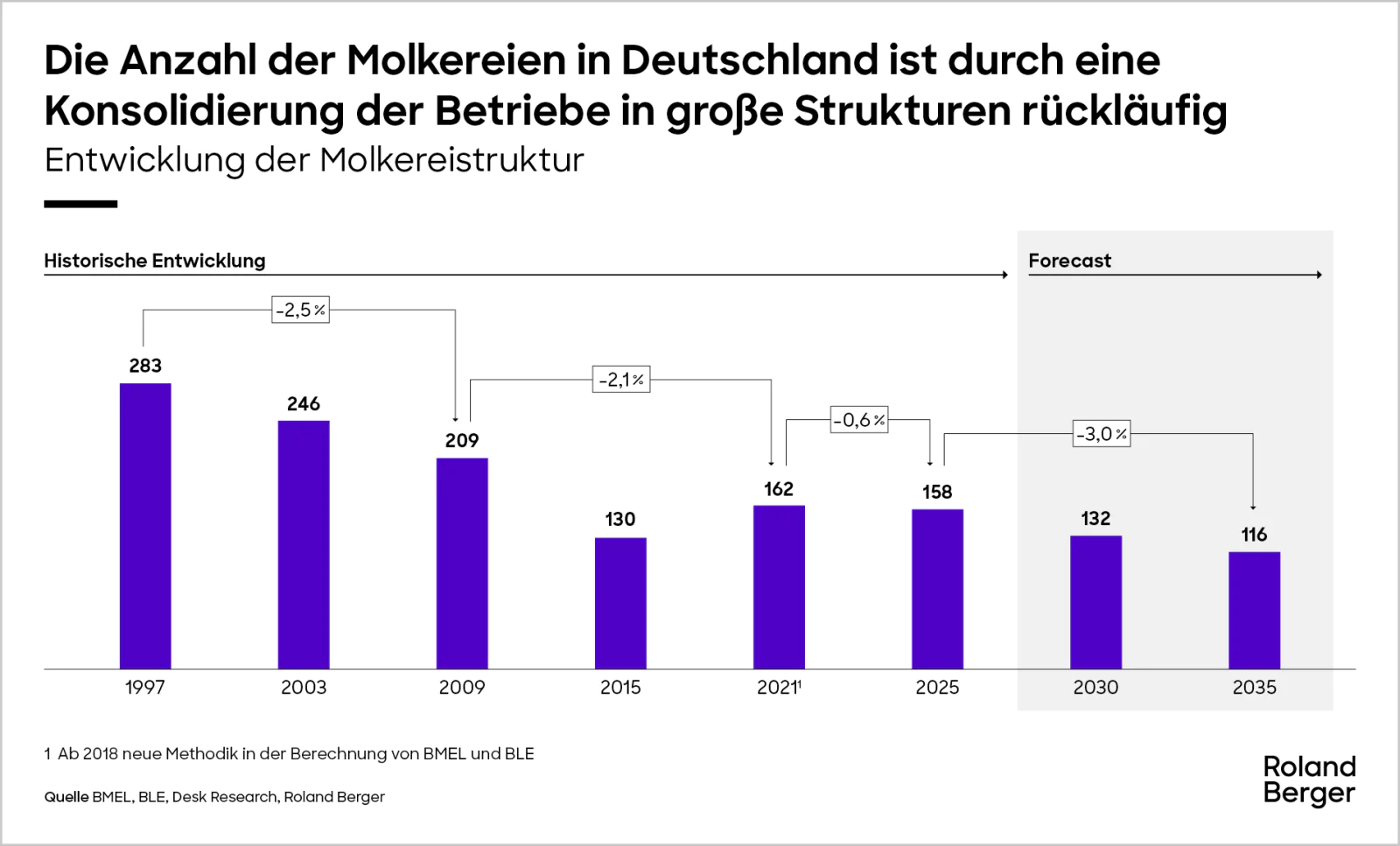

Hypothesis 2: Market consolidation is progressing

Consolidation in the German dairy industry is progressing rapidly. The number of dairy farms has fallen from around 94,000 in 2010 to around 50,000 in 2024 – a reduction of more than 55 per cent in just 13 years. At the same time, total milk production remains stable at around 32 million tonnes. As for processing, the number of dairies has almost halved.

Major mergers, such as the planned merger of Arla Foods and DMK to form Europe’s largest dairy cooperative, illustrate this trend. The authors’ analysis shows that companies need a turnover of at least €250 million to remain relevant in the food retail sector in the long term and to have sufficient bargaining power.

But size alone is not enough. Equally important is clear differentiation through regional presence or a product’s unique functional positioning. Roland Berger supports companies in developing and implementing growth strategies, identifying M&A opportunities, and strategic positioning.

Hypothesis 3: Growth requires restructuring

The profitability speaks for itself: whilst commodity dairy plants often achieve an EBIT margin of less than 2 per cent, specialised dairy plants with differentiated products can achieve margins of between 5 and 10 per cent or more. The greatest growth potential clearly lies outside the saturated mass market: functional dairy products, such as protein drinks, are growing worldwide at an average annual rate of 6 to 8 per cent.

Companies must actively develop new areas of growth. An export share of between 30 and 50 per cent should be a strategic goal for dairy plants operating across several regions. Germany is already a leader in cheese exports. Experts are developing tailored market entry strategies and identifying opportunities for differentiation in attractive product segments.

“To ensure their future viability, it is crucial for dairy companies to secure future growth through strategic partnerships, vertical integration and targeted internationalisation,” says Tobias Kramolowski, a director at Roland Berger.

Hypothesis 4: Swift and enterprising action as a factor for success

A look at the sector’s financial structure reveals a striking difference: whilst privately owned, owner-managed dairies can boast an equity ratio of between 40 and 60 per cent, cooperatives often have only between 15 and 25 per cent. Although cooperatives process around 60–65 per cent of Germany’s raw milk, their purchasing commitments and slow decision-making processes, which often take months or even years, make them significantly less flexible.

Successful dairy plants therefore foster a culture of swift, proactive action: structural optimisation of production and organisation must be actively pursued during periods of economic prosperity, rather than only when a crisis strikes. Speed is a strategic competitive advantage. Roland Berger supports the further development of organisational structures and decision-making processes that ensure flexibility.

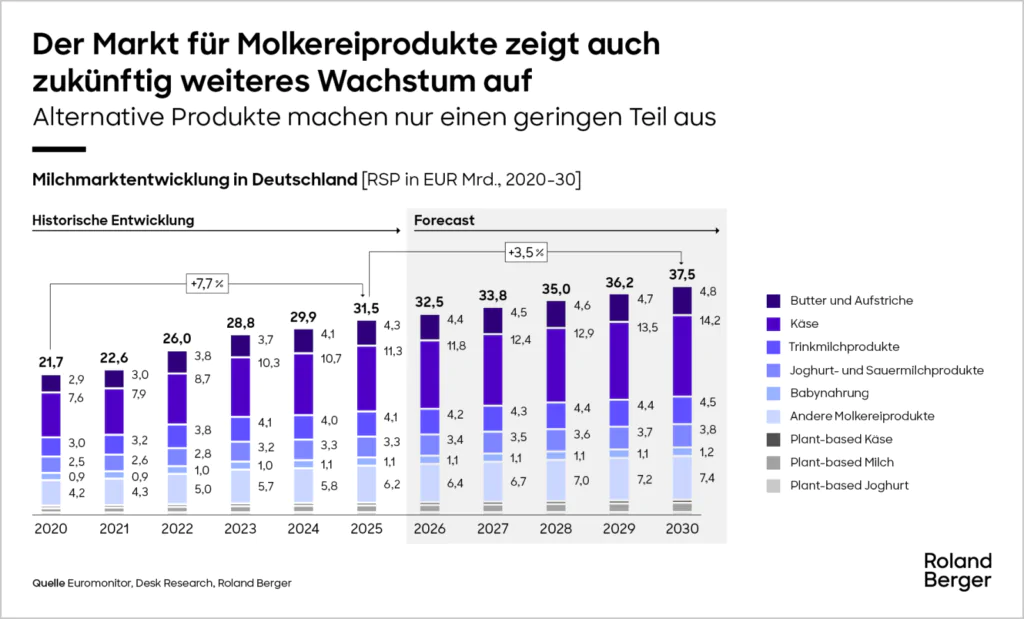

Hypothesis 5: Milk remains an important source of protein

Despite the hype surrounding plant-based alternatives, cow’s milk remains the dominant source of protein in the German diet. With a projected turnover of €30 billion in 2025, Germany is one of the largest markets for dairy products in Europe. Plant-based alternatives currently account for only around 4 per cent of the total market. From a nutritional perspective, cow’s milk has a clear advantage: with approximately 3 g of protein per 100 ml, it significantly outperforms oat milk, which contains around 1 g per 100 ml.

Almost three-quarters of German consumers prefer natural ingredients – a trend that further favours cow’s milk over highly processed plant-based products. Dairy companies must proactively focus on their core business and clearly communicate the obvious nutritional benefits. At the same time, they must constantly monitor the market for alternatives. Roland Berger supports companies in strategically developing their potential across the entire dairy value chain.

“For further growth, it is essential to clearly define the brand’s often hybrid business model – without shying away from difficult compromises,” says Nicolas Wüthrich, Partner at Roland Berber. Zurich Office, Central Europe.

Hypothesis 6: Artificial intelligence will transform all areas of business

Artificial intelligence in the dairy industry is still in its infancy: only 15–20 per cent of German food companies are actively using AI. However, the potential is significant: planning and logistics using artificial intelligence could achieve cost reductions of 10–15 per cent across the dairy industry’s value chain.

Those who do not invest now risk falling behind. A gradual, targeted transformation is the right approach: start with mature applications and systematically unlock efficiency potential in production, the supply chain and procurement. Furthermore, an AI-enabled organisation requires new skill sets. Roland Berger provides specific AI tools, such as the RfP Comparison & Negotiation Agent and the Smart Inventory Optimizer, and supports companies on their journey towards becoming data-driven organisations with the right tools and expertise.

Growth is possible – even in uncertain times.

The German dairy industry is undergoing a period of profound transformation. Alongside undeniable risks, there are also attractive opportunities – for those who are prepared to take decisive action now. Successful dairy companies of the future strategically plan to account for volatility, combine critical mass with genuine differentiation, and consistently develop new avenues for growth.

Source: Roland Berger