As noted by AHDB, the recovery of the commercial dairy markets in the first quarter of 2026 raised hopes of an increase in milk purchase prices and an easing of pressure on farm profitability. However, market signals remain mixed, and in April the dairy fats segment lost a significant portion of its previous gains, indicating that the recovery is fragile.

Wholesale prices in the UK remain under pressure

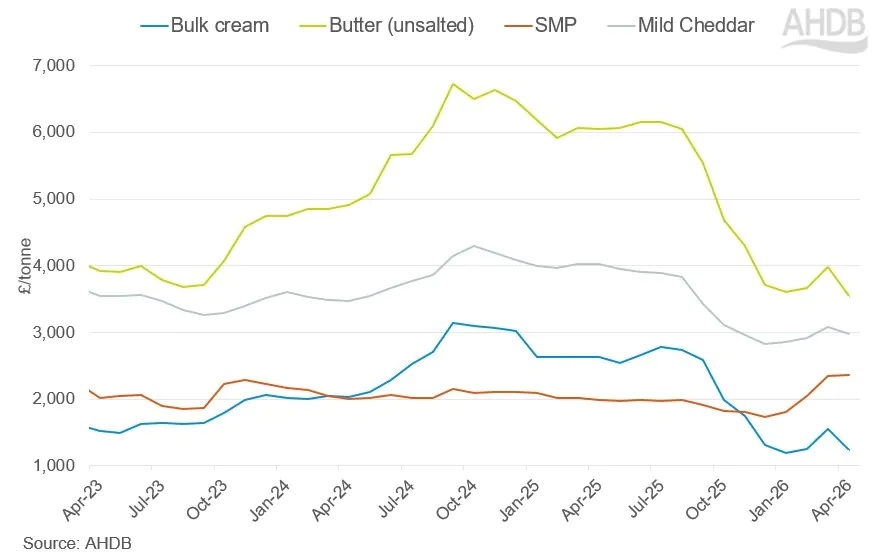

Average wholesale prices in the UK from the start of 2023 to April 2026 show that butter remained the most expensive dairy product, although its price has now fallen to its lowest levels during this period.

All key dairy products — cream, butter, skimmed milk powder (SMP) and soft cheddar — fell sharply in price between late summer 2025 and early 2026. In February and March, the market showed some signs of recovery, but by April, prices for butter, cream and Cheddar had fallen again.

Whey showed the greatest increase at the start of 2026, whilst cream remained the cheapest product throughout the entire period.

Why have the markets moved in the opposite direction?

The main reason for the market’s weakness remains the surplus of milk in the UK and globally, which continues to outstrip demand.

The dairy fats segment came under the greatest pressure. Due to rising supply, prices for cream fell by 20% in April, whilst butter prices dropped to £3,540 per tonne — the lowest level since September 2021.

Compared with last year, the price of cream has fallen by 53%, and that of butter by 41%.

Cheddar also fell by around 3%, although this was partly offset by a rise in whey prices.

The protein trend is driving growth in certain segments

One of the few positive factors in the market remains the high demand for protein. The popularity of functional foods and weight-loss products is driving demand for protein-based dairy ingredients.

That is precisely why whey remains the only product whose price is higher than last year’s.

The market is receiving further support from lower production volumes in the US and competitive global prices, which are boosting exports.

The latest Global Dairy Trade (GDT) auction on 5 May 2026 also confirmed the market’s volatility:

- the price of WMP rose by 2.2%;

- SMP rose by 3.0%;

- butter has fallen in price by a further 2.6%;

- Cheddar fell by 3.6%.

What about prices at farms?

The impact on purchase prices remains unclear.

Some processors began to gradually raise milk prices following an improvement in the situation on the commodity markets in the first quarter of 2026. However, the fall in prices in April may offset these positive developments.

Other companies are holding off on adjusting their prices for the time being, awaiting a clearer signal from the market.

Does the war in Iran play any part?

The war in Iran is not yet the main factor putting pressure on the market, but it may have an indirect impact on exports and production costs.

Due to problems in the Middle Eastern markets, some European and New Zealand products may be redirected to other markets, intensifying competition.

At the same time, the conflict is already having an impact on production costs:

- fertiliser prices have risen by more than a third;

- the cost of diesel fuel is rising;

- Feed prices are starting to rise.

As a result, farmers are facing a double squeeze — lower milk prices and higher production costs.

What can farmers do?

The AHDB advises farmers to keep a close eye on market signals, keep costs under control and plan production strategically, particularly during the spring season.

Milk supplies are already beginning to decline gradually. In the week leading up to 25 April 2026, production fell by 0.3%, and this trend is likely to continue.

Source: AHDB