In 2026, the dairy industry in the US and Europe is operating amid high costs, staff shortages and market volatility, but demand for protein-rich dairy products continues to underpin the sector. A study by McKinsey & Company shows that producers are focusing on protecting margins, innovation in the protein segment and digitalisation.

The eighth annual survey of dairy industry executives, which this year was expanded to include Europe, indicates that the sector is facing significant pressure on costs and profitability, despite rising demand.

The industry is operating under intense pressure

In the early months of 2026, dairy processors in the US and Europe found themselves facing challenging conditions, characterised by:

- the constant rise in costs;

- labour shortage;

- volatility in raw material prices;

- uncertainty in the areas of trade and regulation.

Animal health issues pose an additional risk, including:

- highly pathogenic avian influenza;

- “blue tongue”;

- New World screw worm.

Against this backdrop, consumer demand remains relatively stable, particularly in the protein-rich dairy products segment.

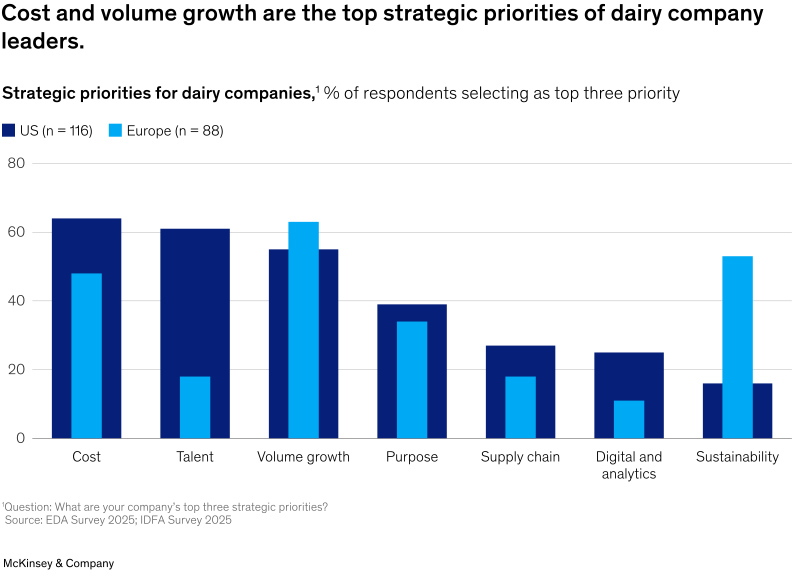

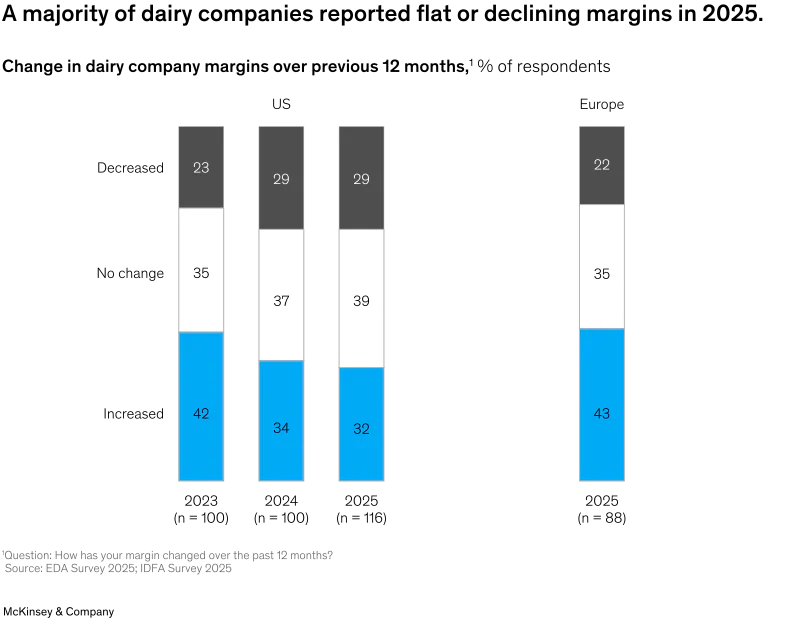

Cost management has become a top priority

In both the US and Europe, cost control has become one of the key strategic priorities.

In the US:

- 65% of companies cited cost management as one of their top three priorities;

- Almost 70% of manufacturers reported stable or lower profit margins in 2025.

In Europe:

- around half of the companies have made cost control a top priority;

- 57% of manufacturers also reported stable or lower profit margins.

To ease the pressure on the company:

- change suppliers;

- optimise their product range;

- are reviewing their sales geography;

- improve operational efficiency.

Volume growth remains a strategic objective

Despite pressure on profitability, most manufacturers continue to focus on growth.

In the US:

- 55% of companies cited increasing volumes as a key priority;

- The dairy industry is investing around $11 billion in new production capacity.

In Europe:

- 65% of respondents also place volume growth at the heart of their strategy;

- At the same time, some companies are expecting restrictions due to a shortage of milk and labour.

Industry leaders note that consumption of dairy products continues to rise, particularly in categories with a high protein content.

The labour shortage remains a problem for the US

In the US, labour shortages remain one of the most pressing challenges:

- 61% of managers cite it as a strategic priority;

- The greatest shortage is among technical specialists and production management staff.

American companies are actively:

- work in partnership with colleges;

- are expanding their internship programmes;

- are investing in staff training.

In Europe, the labour shortage is less acute at the factory level, but is felt much more keenly on farms due to the ageing farming population and issues surrounding business succession.

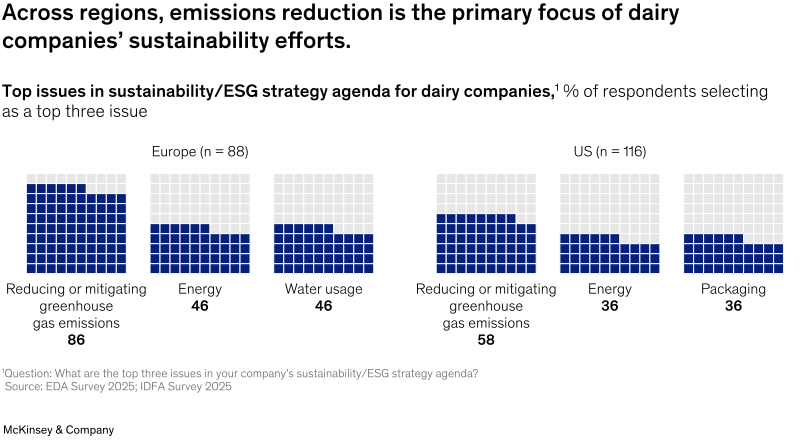

Sustainable development: Europe and the US have different approaches

In Europe, sustainable development remains one of the top priorities:

- 53% of companies include ESG among their top three strategic priorities;

- 86% cite reducing greenhouse gas emissions as a key priority.

In the US:

- only 16% of executives rank ESG among their top priorities;

- The main emphasis is placed on the economic viability of environmental solutions.

The most common initiatives:

- energy efficiency;

- logistics optimisation;

- reducing losses;

- reduction in methane emissions;

- improvements to the packaging.

At the same time, many managers acknowledge that consumers are not prepared to pay significantly more for ‘green’ dairy products.

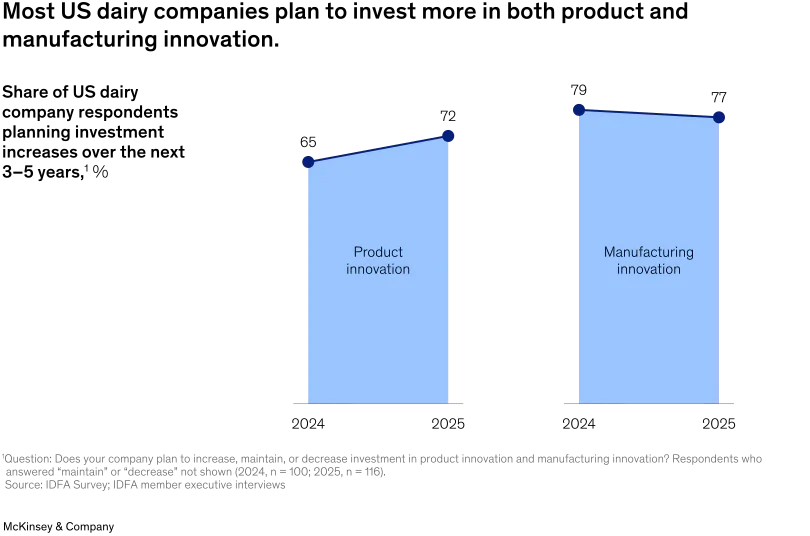

Protein has become the main driver of innovation

The protein segment is currently the most important area of development in the dairy industry.

In the US:

- 88% of executives cite protein as the main consumer trend.

In Western Europe:

- The high-protein dairy products segment grew by an average of 17% annually between 2019 and 2024.

Companies are actively investing in:

- high-protein drinks;

- functional snacks;

- sir;

- yoghurts;

- protein ingredients.

Protein is increasingly being seen not as a short-term trend, but as a fundamental growth strategy for the industry.

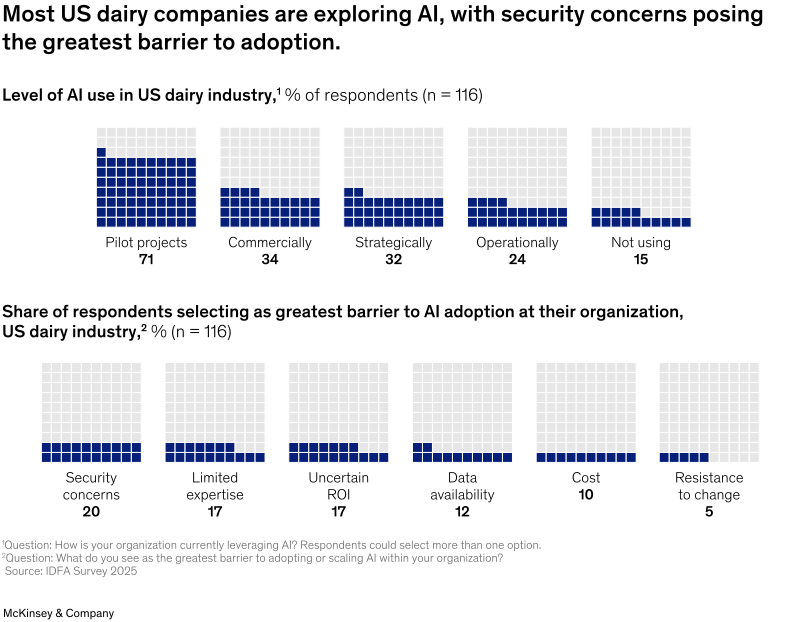

Artificial intelligence is gradually making its way into the dairy industry

Around 80% of US companies are already testing or using artificial intelligence and analytics tools.

Main areas of application:

- forecasting;

- maintenance;

- planning;

- administrative efficiency;

- knowledge management.

However, most companies are still at the pilot project stage.

Main barriers:

- security risks;

- uncertain return on investment;

- lack of experience.

European companies are adopting AI even more cautiously, primarily as a tool for improving efficiency rather than for business transformation.

Key priorities for the dairy sector in 2026

According to industry leaders, success in 2026 will depend on:

- margin protection;

- disciplined cost management;

- the development of protein products;

- stabilising the talent pool;

- practical ESG solutions;

- targeted investment in artificial intelligence and digitalisation.

Despite market volatility, the dairy sector remains optimistic about long-term demand, particularly in the high-protein segment.

Source: McKinsey & Company