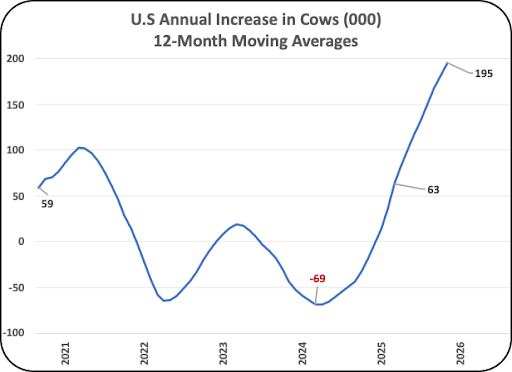

The US milk cow population has grown significantly through 2025 and into Q1 2026. As John Geuss notes in his blog on Milk Pay reports, a 3% rise in the herd against flat domestic consumption is forcing the industry to seek export markets — and keeping producer prices low.

Domestic consumption of most dairy products is not growing, yet the trend toward more cows shows no signs of slowing. The result is a structural need to export US dairy products, while wholesale — and therefore producer — prices remain depressed.

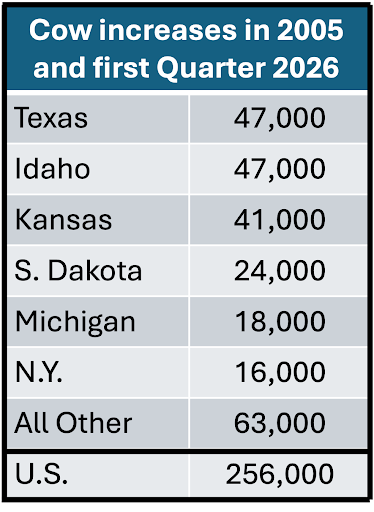

Most of the states driving herd growth are in the north, where the climate suits dairy cattle, and many fall outside Federal Order pricing. Washington is the only state with a notable herd decline (-20,000 cows, -8%). New processing plants have been built across the country, but existing facilities have not been retired — adding to total milk output.

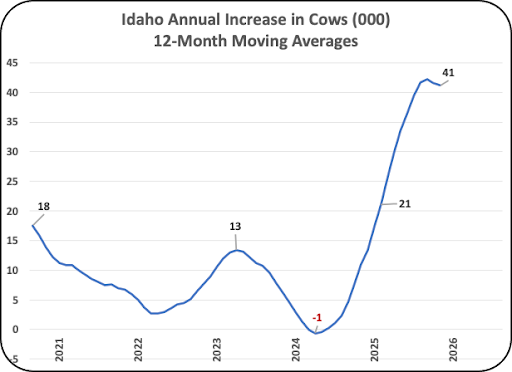

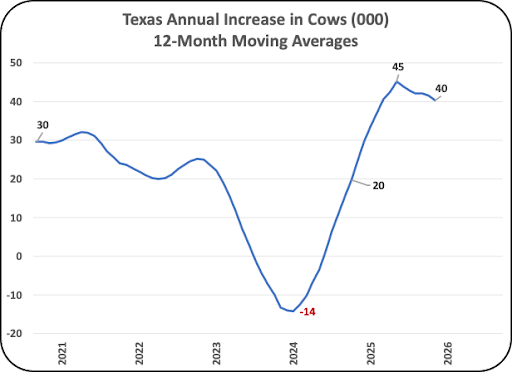

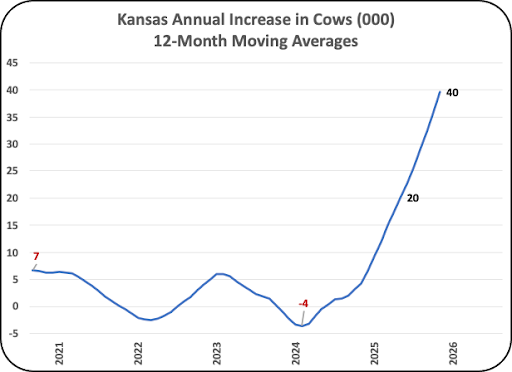

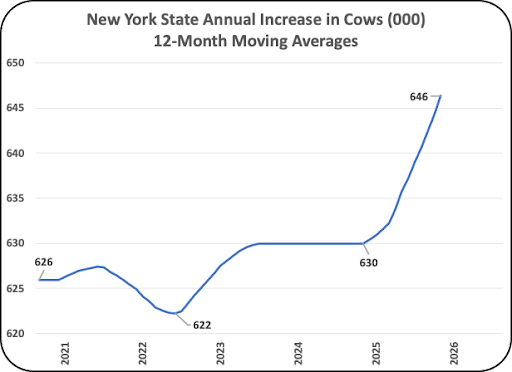

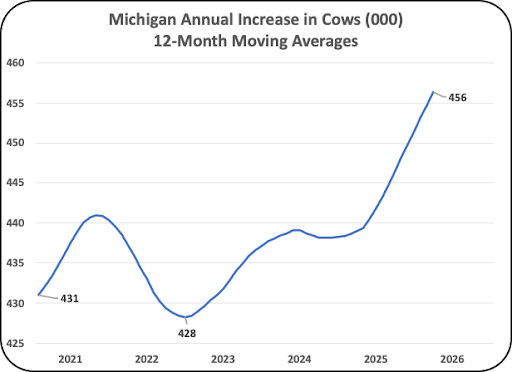

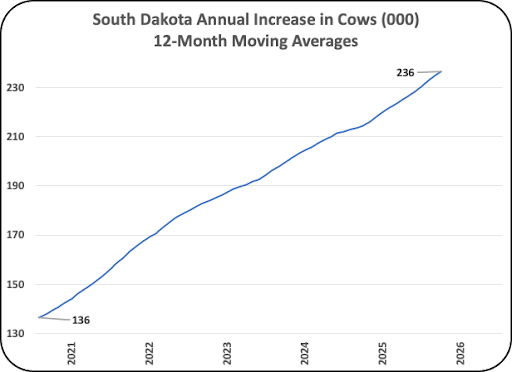

Key state snapshots: Texas (+7% YTD) rebuilt its herd after H5N1 culling and drought in 2023–24 but is now seeing a gradual slowdown. Idaho (+7% YTD) benefited from new Chobani capacity and a favourable agricultural climate. Kansas led growth at +17% YTD, adding 41,000 cows, driven by new processing investment. South Dakota’s herd is up 71% over the full charted period — a steady, long-term climb fuelled by new cheese plants. Michigan (+4% YTD) consistently records the highest milk-per-cow of any state. New York (+3% YTD) is supported by new facilities such as fairlife.

Summary

The US dairy industry is changing rapidly. New processing plants require strategically located new herds. There is too much milk for domestic consumption. When will supply and demand find equilibrium? More change is coming — and to survive, adaptation is essential.

Source: Milk Pay